How to Set Billing Rates for Architecture & Engineering Firms:

Build Rates From Your Numbers, Not the Market's

Most A/E firms set billing rates based on what competitors charge or what clients seem willing to pay. Neither approach connects rates to what it actually costs to run the firm. Here's how to calculate billing rates from your real overhead factor and target multiplier — so every proposal starts from a defensible, profitable number.

Why Most A/E Billing Rates Are Wrong

Billing rates in A/E firms are usually set one of two ways.

The first is market comparison — find out what similar firms charge and land somewhere in that range. The second is intuition — raise rates when it feels like the market will bear it, hold them when it doesn't.

Neither approach connects rates to what it actually costs to run the firm.

The result is a billing rate that may cover costs in a good year and fail to in a slower one — with no clear way to know which situation you're in until the P&L closes.

The Formula-Based Approach

A billing rate built from first principles has three components:

Raw Labor Cost × (1 + Overhead Factor) × Target Multiplier = Billing Rate

Each component has a specific job:

- Raw labor cost is what the firm pays the employee per hour — salary divided by annual billable hours

- Overhead factor grosses that cost up to reflect the true cost of keeping that person on staff and running the firm

- Target multiplier adds the margin the firm needs to be profitable

A billing rate built this way is not a guess. It is a minimum — the rate below which the firm cannot deliver that person's work profitably at the target multiplier.

→ Read: Overhead Factor Explained: The Missing Link Between Busy and Profitable

→ Read: The 3.0 Rule: Why Your Projects Aren't as Profitable as You Think

A billing rate is not a market position. It is a cost recovery floor.

What competitors charge tells you whether your rate is competitive. It tells you nothing about whether your rate covers your costs. Those are two different questions — and only one of them determines whether your firm makes money.

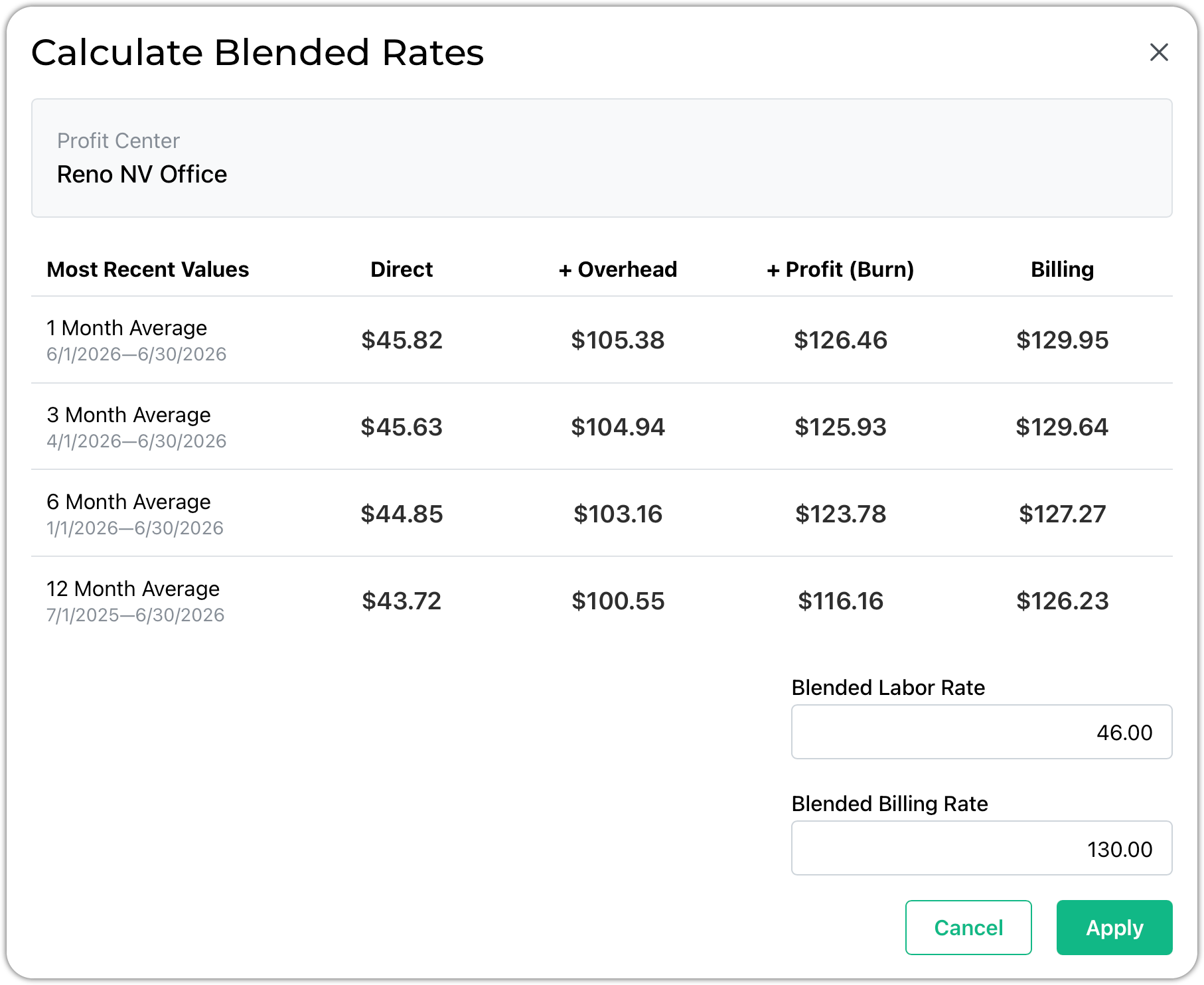

How to Calculate Your Billing Rate

Step 1: Calculate raw labor cost per hour

Start with the employee's annual salary. Divide by their target annual billable hours — not total working hours.

If a staff member earns $72,000 per year and is expected to log 1,600 billable hours annually, their raw labor cost is $45.00 per hour.

Most firms use 1,600–1,800 billable hours as an annual target depending on role and firm structure. Using total working hours (2,080 for a full-time employee) overstates billable capacity and produces a cost per hour that is too low.

Step 2: Apply your overhead factor

Multiply raw labor cost by (1 + overhead factor).

If your overhead factor is 1.65, every dollar of direct labor carries $1.65 in overhead. The fully loaded cost per hour for that $45.00 employee is:

$45.00 × (1 + 1.65) = $45.00 × 2.65 = $119.25 per hour

That is what it actually costs the firm to put that person on a project for one hour — before any profit is earned.

→ Read: Calculate True Project Cost with Your Overhead Factor

Step 3: Apply your target multiplier

Multiply the fully loaded cost by your target net multiplier.

At a 3.0 multiplier, the minimum billing rate for that employee is:

$45.00 × 3.0 = $135.00 per hour

Note that the multiplier is applied to raw labor cost, not to the fully loaded cost. The overhead factor is already embedded in what makes 3.0 the right target — it is the spread needed to cover overhead and produce a sustainable operating margin.

Step 4: Check against market rates

Once you have your formula-based minimum, compare it to what the market supports.

If your minimum is $135 and the market comfortably supports $155–175 for that role, you have pricing room. If your minimum is $150 and the market tops out at $140 for similar work in your region, you have a cost structure problem that no amount of rate-setting will solve — the overhead factor or salary level needs to be addressed directly.

A worked example:

Staff member salary: $80,000

Target billable hours: 1,600/year

Raw labor cost: $50.00/hour

Overhead factor: 1.70

Fully loaded cost: $50.00 × 2.70 = $135.00/hour

At 3.0 multiplier: $50.00 × 3.0 = $150.00/hour minimum billing rate

If that person is currently billed at $125/hour, the firm is losing ground on every hour they log — regardless of how busy they are.

Common Billing Rate Mistakes in A/E Firms

Setting one rate per person and never revisiting it

Salaries increase. Overhead shifts. The firm adds staff, moves offices, or takes on more benefits. Any of those changes affect the overhead factor — and therefore the minimum billing rate.

Firms that set rates once and hold them for two or three years are often billing below their actual cost floor without realizing it. The rate that covered costs in year one may not cover them in year three.

A practical rule: recalculate minimum billing rates any time the overhead factor is updated — ideally annually from a trailing 12-month P&L.

Using the same billing rate regardless of project type

A firm's standard billing rate may be appropriate for most work — but some project types carry higher overhead, more coordination complexity, or longer phase durations that compress the effective multiplier.

Firms that apply a single rate across all project types are subsidizing their less efficient work with their more efficient work, without knowing which is which.

Discounting without understanding the multiplier impact

When a firm offers a 10% rate discount to win a project, it feels like a modest concession. In multiplier terms, it may be the difference between 3.0 and 2.7 — a meaningful margin reduction on every hour logged.

Rate discounts should be evaluated against their multiplier impact, not just their percentage. A project that requires a discount to win may not be worth winning at that rate.

Setting rates for principals too low

Principal time is often underpriced relative to its actual cost. Principal salaries are high, their billable hours are typically lower due to business development and firm management responsibilities, and their overhead allocation per billable hour is therefore higher.

A principal billed at the same rate as a senior associate — or worse, at a rate set years ago when the firm was smaller — is almost certainly generating a below-target multiplier on every hour they bill.

The billing rate conversation is easier than the write-off conversation.

Raising billing rates by $15–20 per hour is uncomfortable for one quarter. Discovering that the firm has been running below break-even for two years because rates never kept pace with overhead is a different kind of uncomfortable — one with fewer options attached to it.

How Billing Rates Connect to the Rest of Your Financial Metrics

Billing rates are the starting point for every other financial metric in the chain.

If rates are set below the cost recovery floor, no amount of utilization improvement, WIP management, or realization discipline can fully compensate. The math is against the firm from the moment the proposal goes out.

Billing rates and utilization

A firm with low utilization needs higher billing rates to recover the same overhead across fewer billable hours. When utilization drops — seasonally, during a slow period, or after a key project closes — the gap between fixed overhead and billable recovery widens. Rates that worked at 80% utilization may not work at 65%.

→ Read: Utilization Rate for A/E Firms

Billing rates and realization

A billing rate is only as effective as the realization rate behind it. A $150/hour rate that realizes at 85% is effectively a $127.50/hour rate. Firms that have worked carefully to set defensible rates and then absorb write-offs at billing time are undermining their own rate structure.

→ Read: Realization Rate for A/E Firms

Billing rates and net multiplier

The net multiplier is the summary metric that reflects whether billing rates, utilization, and realization are all working together. A firm targeting 3.0 but running 2.6 has a problem somewhere in that chain — and billing rates are the first place to look.

What Good Billing Rate Management Looks Like

A firm managing billing rates well can answer these questions at any point in the year:

- What is the minimum billing rate for each staff member at our current overhead factor?

- When did we last recalculate rates — and has overhead shifted since then?

- Which staff members are currently billed below their cost recovery floor?

- What is the multiplier impact of the rate discounts we've offered this year?

- Are principal billing rates keeping pace with their actual cost per billable hour?

These are not complicated questions. They are just questions most firms never ask — because the rate was set once, filed away, and treated as a fixed feature of how the firm operates rather than a number that needs to stay current.

→ Read: Financial Metrics for A/E Firms: The KPIs That Actually Predict Profitability

→ Read: Stop Measuring Profit the Wrong Way

Cut Your Billing Time by 60% Within 90 Days — Or We Refund Every Penny

We're so confident BaseBuilders will transform your billing process that we're putting our money where our mouth is.

BaseBuilders’ easy-to-use software is specifically designed to help small to mid-sized firms track time, manage projects, stay on top of expenses, and more. We’ll handle the invoicing for you so you can focus on growing your firm and designing wonderful spaces.