How to Calculate Your Overhead Factor

The Number Every A/E Firm Needs and Most Can't Produce

The overhead factor tells you what your work actually costs — not just what you paid in salaries, but what every billable hour carries in overhead burden before a dollar of profit is added. Most A/E firms either don't know their overhead factor or calculated it from a P&L that wasn't structured to support the calculation. Here's the right methodology, with a real P&L and real numbers throughout.

What the Overhead Factor Actually Measures

The overhead factor is a ratio. It measures the overhead the firm incurs per dollar of direct labor.

Formula: Overhead ÷ Direct Labor = Overhead Factor

If a firm has $499,625 in overhead and $310,000 in direct labor, the overhead factor is 1.61.

That means: for every dollar spent on direct labor — labor charged to client projects — the firm incurs $1.61 in overhead costs. Rent, insurance, indirect payroll, subscriptions, marketing, professional development, bank charges — all of it, expressed as a ratio against the direct labor that drives revenue.

That ratio is what makes pricing defensible. A staff member costing $47/hour in direct labor costs $75.67/hour when overhead is applied. Adding a 3.0 target multiplier produces a minimum billing rate of $141/hour. That is the floor — the rate below which the firm cannot deliver that person's work at the target margin. Below it, the firm is subsidizing the project from its own equity.

Without the overhead factor, billing rates are set based on gut feel, market comparisons, or industry benchmarks that may not reflect the firm's actual cost structure. All three produce rates that may look competitive and be quietly unprofitable.

Why most firms don't know their overhead factor

The calculation requires two specific figures that most A/E firm P&Ls are not configured to produce: total overhead — all firm costs except direct labor — and direct labor — payroll dollars specifically charged to client projects.

When payroll sits in a single account — as it does by default in QuickBooks — the split between direct and indirect labor is invisible. The overhead factor cannot be calculated because the denominator and one component of the numerator are permanently combined in the same account.

Fixing the P&L structure is the prerequisite. The calculation itself is straightforward once the books are correctly configured.

→ Read: How to Separate Direct and Indirect Labor in QuickBooks

The overhead factor cannot be calculated from a P&L where payroll sits in a single account.

The calculation is simple. The prerequisite — separating direct from indirect labor in the books — is what most firms have never done.

The Correct P&L Structure for the Calculation

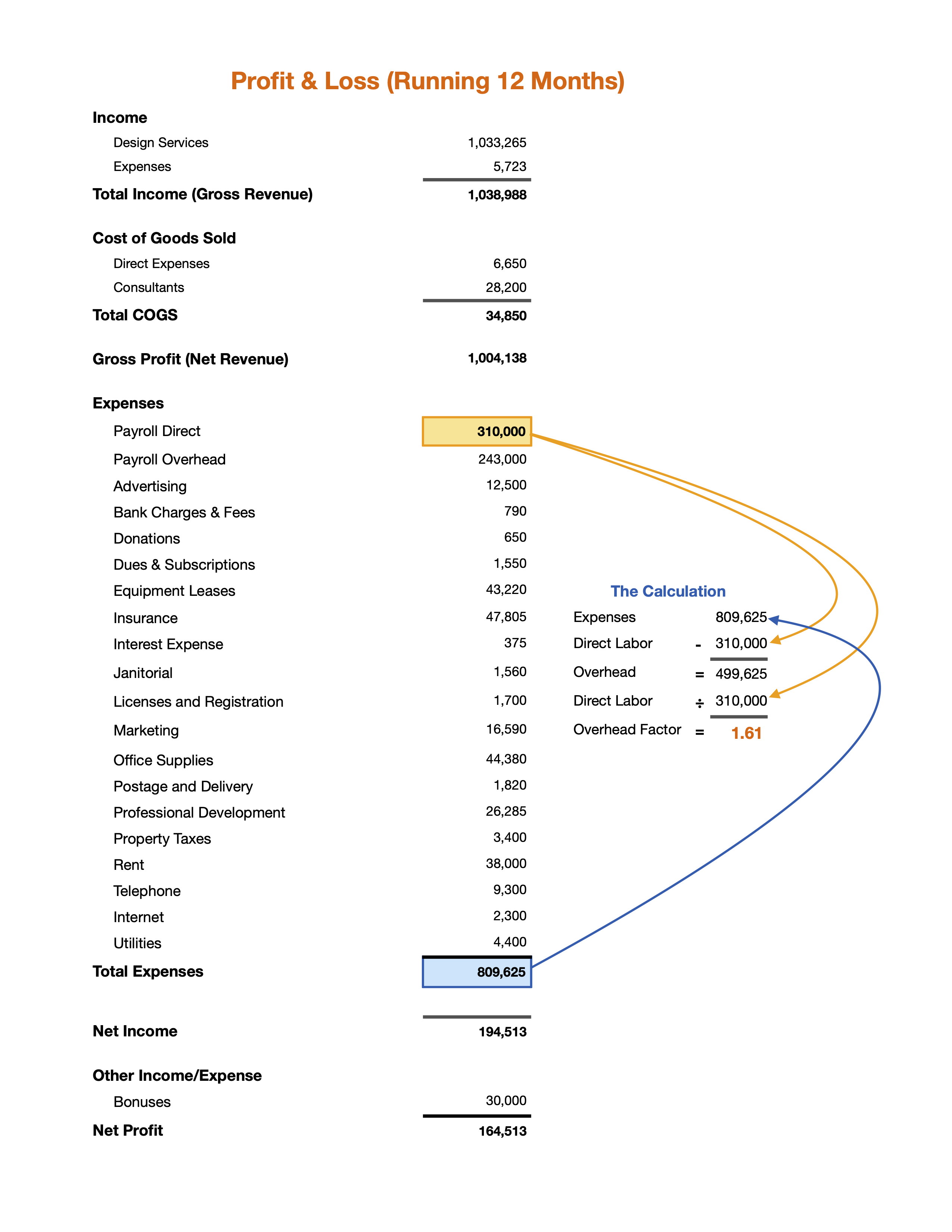

The overhead factor calculation requires a P&L organized in a specific way. Here is what that structure looks like — using real figures from an actual A/E firm.

Income flows in at the top as gross revenue. Design services of $1,033,265 plus other income of $5,723 produces total gross revenue of $1,038,988.

Cost of Goods Sold contains two items only: direct expenses of $6,650 and consultant fees of $28,200, for total COGS of $34,850. Direct labor is not here. This is the most common structural error in A/E firm accounting — when direct labor sits in COGS, gross profit no longer equals net revenue and the overhead factor calculation requires manual reconstruction.

Gross Profit — Net Revenue is $1,004,138. This is the correct denominator for every A/E firm profitability ratio. It represents what the firm actually retains after paying for consultant pass-throughs and direct project expenses.

Expenses contain all operating costs, organized with two critical payroll lines kept separate:

Payroll Direct is $310,000 — the compensation paid for hours charged to client projects. This is direct labor and the denominator in the overhead factor calculation.

Payroll Overhead is $243,000 — compensation paid for all other firm time. Administration, marketing, management, internal meetings, business development, training.

The remaining expenses — advertising $12,500, bank charges $790, etc. — bring total expenses to $809,625.

Three structural elements make this P&L suitable for the overhead factor calculation. Consultants and direct expenses are in COGS, and direct labor is not. Payroll is split into two visible, separate accounts. All overhead costs are correctly classified in expenses. Now, with some simple grade school math, you can calculate the overhead factor.

We can also see that this firm has a 19.37% pre bonus net profit on net revenue.

→ Read: Chart of Accounts for Architecture and Engineering Firms

→ Read: Net revenue vs Gross Revenue

The overhead factor calculation is three lines of arithmetic.

The work is in configuring the P&L correctly so those three lines produce accurate inputs — not in the math itself.

The Calculation Step by Step

With the P&L correctly structured, the overhead factor calculation follows directly.

Step 1: Identify total expenses

Total Expenses = $809,625

This is every cost of running the firm for the trailing 12-month period — all payroll, rent, insurance, subscriptions, marketing, equipment, and every other operating expense.

Step 2: Subtract direct labor

Direct Labor (Payroll Direct) = $310,000

$809,625 minus $310,000 equals $499,625 in Overhead.

Overhead is everything the firm spends that is not direct labor. It includes indirect payroll of $243,000, rent of $38,000, insurance of $47,805, equipment leases of $43,220, and every other cost of keeping the firm operational.

Step 3: Divide overhead by direct labor

$499,625 divided by $310,000 equals an Overhead Factor of 1.61.

Every dollar of direct labor this firm spends carries $1.61 in overhead. The true cost of delivering one hour of direct labor work is not $47 — it is $47 multiplied by 2.61, equaling $122.67. That fully loaded cost is what billing rates and project fees must be built from.

Why the trailing 12-month P&L is essential

The overhead factor must be calculated from a trailing 12-month P&L—not a single month, not a calendar year that ended six months ago, and not an estimate based on the current run rate.

Several overhead costs are irregular or seasonal — insurance renewals, annual subscriptions, property taxes, year-end bonuses, and professional development expenses. In any given month, some of these may be present and others absent. A single month's P&L produces an overhead factor that is either artificially high or artificially low, depending on which irregular expenses fell in that period.

A trailing 12-month figure — updated each time a new pay period is recorded — smooths these variations and produces a number that reflects the firm's true cost structure across a complete operating cycle. It is the only basis for an overhead factor that can be applied with confidence to current proposals and billing rates.

What the overhead factor is not

The overhead factor is not the same as an overhead percentage. A common error is to divide overhead by gross or net revenue — producing a percentage that looks like a meaningful metric but drives no useful downstream calculation. The overhead factor is always overhead divided by direct labor. That specific ratio is what connects to the billing rate formula and the net multiplier benchmark.

The overhead factor is also not a fixed industry standard. It varies by firm size, staffing mix, geographic market, and business development intensity. A small firm with heavy principal involvement in non-billable business development will carry a different overhead factor than a larger firm with dedicated marketing staff and a higher utilization rate across technical staff. Industry benchmarks — typically ranging from 1.4 to 1.8 for well-run A/E firms — are useful reference points, not targets. The firm's own number is what matters for pricing.

→ Read: Overhead Factor Explained: The Missing Link Between Busy and Profitable

The overhead factor is not an industry benchmark to match.

It is a firm-specific ratio that changes when costs, staffing, and utilization shift. A number calculated eighteen months ago is leading to proposals priced against a cost structure that may no longer exist.

How Often to Recalculate — and What Changes It

The trailing 12-month P&L updates each month as new expenses are recorded and old ones roll off. In theory, the overhead factor could be recalculated monthly from that updated figure. But nobody is going to do this — and frankly, it isn't necessary. The overhead factor moves in small increments between periods unless something significant changes in the firm's cost structure. We recommend updating it every three to six months. That is close enough.

It is also worth being clear about what the overhead factor is and is not. It is an estimate of how much overhead a given project or hour of direct labor should carry — a planning and pricing tool built from real data. It is not down-to-the-penny job costing. The goal is a number that is current enough to produce defensible billing rates and fee proposals, not one that accounts for every dollar of overhead allocated to every project in real time. Good enough and current is more useful than precise and stale.

What causes the overhead factor to change

Any significant change in the firm's cost structure moves the overhead factor. The most common causes:

New hires — adding staff increases both direct labor (if the new hire is billable) and overhead labor (their non-billable time). Whether the overhead factor rises or falls depends on the new hire's utilization rate — whether they add more direct labor or more overhead relative to their total cost.

Salary increases — across-the-board increases raise both direct and indirect labor proportionally, leaving the ratio relatively stable. Increases concentrated in overhead staff — administration, marketing, management — raise the overhead factor.

Lease renewals and rent increases — rent is a pure overhead cost. A significant lease increase raises overhead without affecting direct labor, moving the factor up.

Changes in utilization — if the team's billable percentage drops, more time goes toward non-billable activities, direct labor decreases relative to total payroll, and the overhead factor rises. This is the direct connection between utilization and pricing: a firm that becomes less efficient at converting labor to billable work needs higher billing rates to cover the same overhead — or it compresses margin.

Business development intensity — a period of heavy business development or proposal writing shifts time from direct to overhead categories, raising the factor temporarily.

When to review billing rates

Beyond the rolling update, a deliberate review of billing rates built on the overhead factor is warranted whenever a significant hire or departure changes the staffing mix, a lease or major cost changes materially, utilization is trending in either direction, or a new service line changes the typical direct/indirect labor split.

How the overhead factor connects to the rest of the financial picture

Once current and accurate, the overhead factor anchors three critical calculations.

The minimum billing rate for any staff member is their raw labor cost per hour multiplied by one plus the overhead factor, multiplied by the target multiplier. At an overhead factor of 1.61 and a 3.0 target multiplier, a staff member with a raw labor cost of $47/hour has a minimum billing rate of $141/hour.

The true project cost for any phase is the direct labor hours multiplied by the raw labor rate multiplied by one plus the overhead factor. This is the cost floor below which the phase cannot be delivered profitably regardless of how efficiently the team works.

The break-even multiplier is simply one plus the overhead factor. At 1.61, the break-even is 2.61 — the multiplier at which the firm covers all costs with zero profit. A net multiplier below 2.61 means the firm is losing money on the work. Between 2.61 and 3.0 means the firm is covering costs but generating below-target profit. Above 3.0, the firm is performing at or above the standard A/E profitability benchmark.

The overhead factor is not just a pricing input. It is the lens through which every revenue figure in the firm gets evaluated.

→ Read: Utilization Rate for A/E Firms

→ Read: How to Set Billing Rates for Architecture & Engineering Firms

→ Read: Financial Metrics for A/E Firms

Cut Your Billing Time by 60% Within 90 Days — Or We Refund Every Penny

We're so confident BaseBuilders will transform your billing process that we're putting our money where our mouth is.

BaseBuilders’ easy-to-use software is specifically designed to help small to mid-sized firms track time, manage projects, stay on top of expenses, and more. We’ll handle the invoicing for you so you can focus on growing your firm and designing wonderful spaces.